Risk Management (MSQF)

Spring, 2022

10 points of each question.

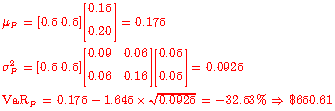

1. Assume two stocks A and B whose return (i.e. percentage) means and variance-covariance matrix are as follows:

![]() and

and ![]()

If each stock is invested $1000. What is the 5% parametric VaR in percentage terms and in dollar

terms? [Note that portfolio variance is

![]() where

where ![]() represents a vector

of weights.]

represents a vector

of weights.]

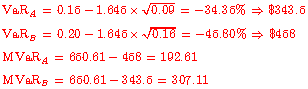

2. (cont’ed) What is the marginal VaR for A and for B?

3. A historical VaR is being calculated. A 100-observation series has been calculated and the worst 10 observations are reported below:

|

-1.338784202 |

|

|

-1.534551838 |

|

|

-1.555734181 |

|

|

-1.616927984 |

7 |

|

-1.628916188 |

6 |

|

-1.646193024 |

5 |

|

-1.675494734 |

4 |

|

-2.042007139 |

3 |

|

-2.150729439 |

2 |

|

-2.281698481 |

1 |

The value of -1.616927984 is ?% VaR? Justify your answer. 7%VaR (or 93% VaR)

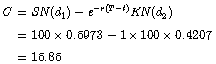

4. You own a portfolio of 1 stock and 1 at-the-money option

(on the same stock). The information of

the stock is: ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() . The option value is

computed as:

. The option value is

computed as:

Now, you need to calculate (dollar) VaR of your

portfolio. The change of value of your

portfolio can be computed as (where ![]() is the delta of your

call):

is the delta of your

call): ![]()

What is the 5% parametric VaR?

![]()

5. OTC derivatives reached the peak in 2008 (prior to the crisis) at $600 trillion while the exchange-traded derivatives has never exceeded $60 trillion. McCarran-Ferguson Act of 1945 stated that insurance companies are regulated at the state level. Risk measures satisfying four conditions (i.e. monotonicity, translation invariance, homogeneity, and subadditivity) are referred to as coherent risk measures. Investment-grade securities (e.g. corporate bonds) are those rated BBB or higher.

6. What is the role of a clearing house. See book